Pulse24 Original

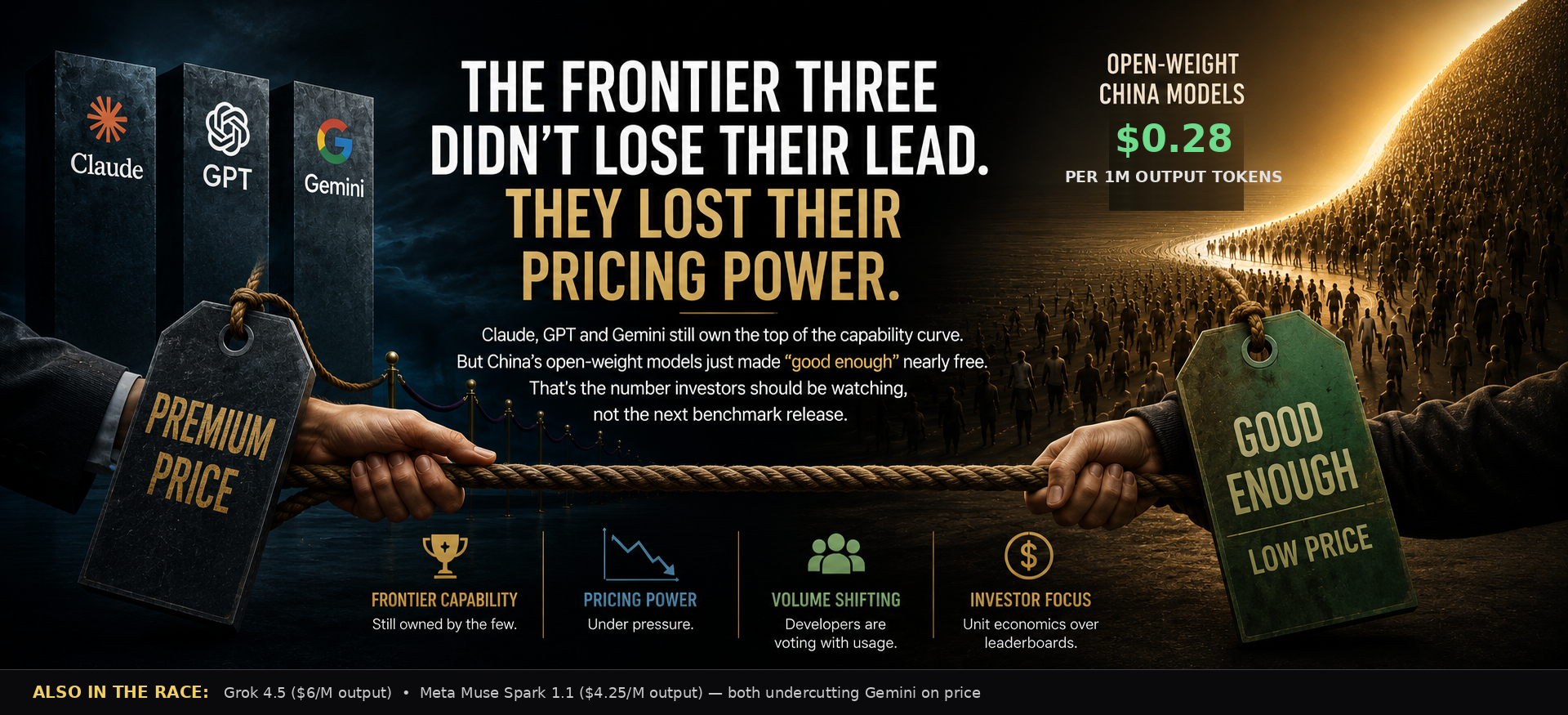

The Frontier Three Didn't Lose Their Lead. They Lost Their Pricing Power.

Claude, GPT and Gemini still own the top of the capability curve. China's open-weight labs just made "good enough" nearly free, and that's the number investors should be watching, not the next benchmark release.

July 17, 2026

The market is asking the wrong question. Everyone wants to know who has the smartest AI. Investors should be asking who still has the power to charge a premium for it.

Claude, GPT and Gemini still sit at the top of the capability curve today. The more important question is whether staying at the top still lets these three labs charge what they used to.

Where each frontier lab actually wins

Start with what each lab is genuinely best at, because "best AI" stopped being a single answer months ago.

Claude holds the clearest lead in agentic coding and long-chain reasoning. On SWE-bench Verified, the benchmark that tests whether a model can actually fix real software bugs end to end, Anthropic's models occupy the top three spots industry-wide. That's the difference between assisting engineers and completing engineering work autonomously.

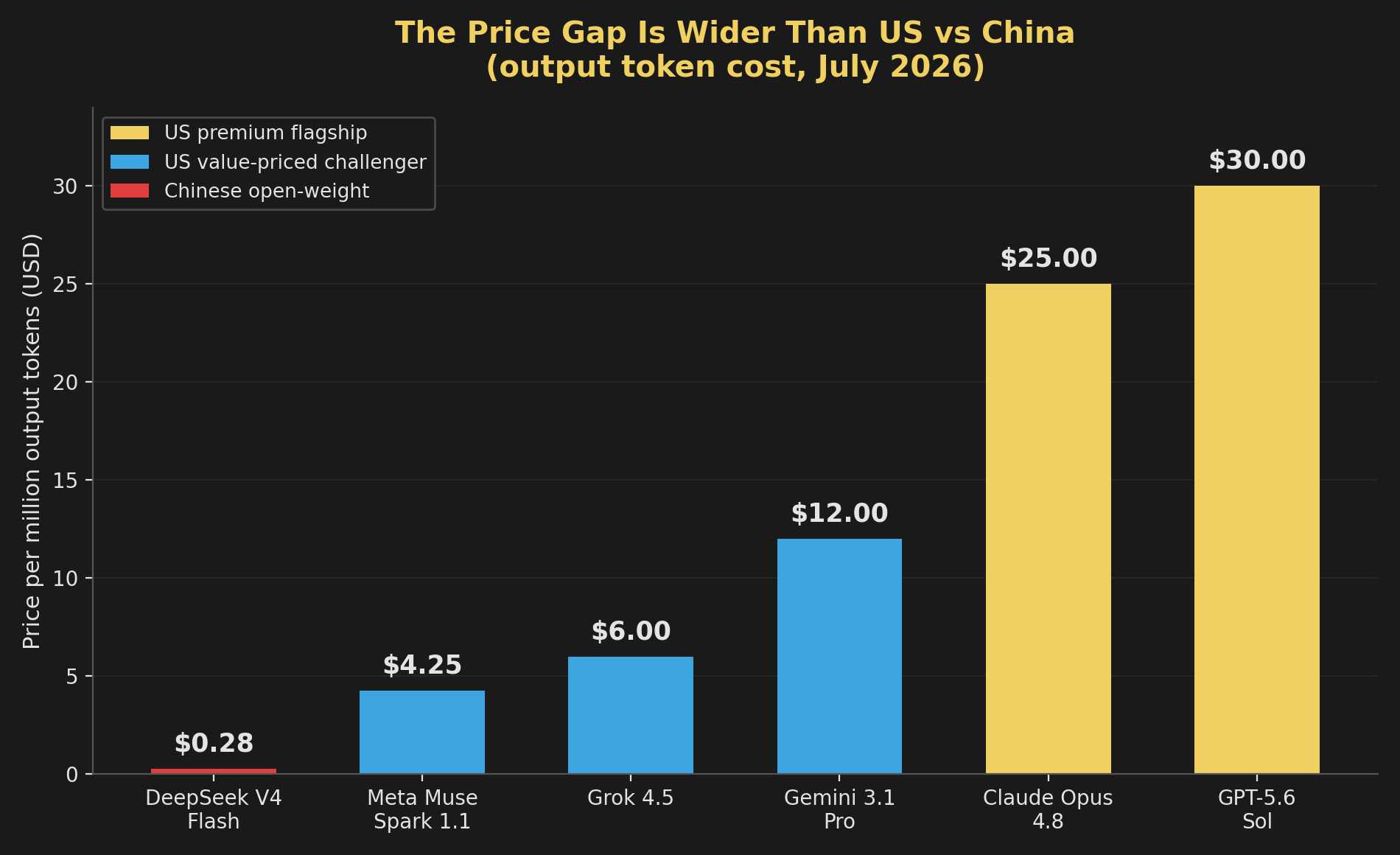

Gemini wins on price-to-performance among the proprietary tier. It posts a strong GPQA Diamond score (a graduate-level science reasoning test) while generally pricing below both rivals for comparable reasoning workloads, currently around $12 per million output tokens against $25 to $30 for its two closest competitors.

GPT holds the edge on the single hardest math and science problems in existence. FrontierMath Tier 4, built specifically to be nearly unsolvable, is where OpenAI's models pull furthest ahead, roughly double the next-best verified score.

No lab wins everywhere. Claude's weak spot is upfront cost, sitting at the top of the market per token. Gemini still trails on the very hardest structured reasoning chains despite leading on broader science reasoning. GPT's gap is access rather than ability: its newest flagship tier launched behind a gated preview tied to a government safety review, and carries the highest output price of the three once fully released.

We've seen this movie before

Nvidia may still build the fastest AI chips. That doesn't mean every inference workload needs Nvidia's fastest chip. Custom silicon from Google, Amazon and a handful of others already runs a meaningful share of production inference at a fraction of the cost, precisely because most of that workload doesn't require the ceiling of performance, just enough of it.

Every technology industry eventually splits into two businesses this way. One owns performance. The other owns volume, and volume is where the money actually sits once a technology matures. History suggests performance leadership and pricing leadership rarely stay the same business forever. Once capability crosses the line into good enough for most customers, competition shifts away from benchmarks and toward cost. AI looks like it is entering that phase.

The data that proves it's already happening

Chinese-origin models have held more than 30% of weekly token volume on OpenRouter, the largest AI model routing platform, every week since February 2026, peaking at 46% by early July. A year earlier that share was under 5%. That's developers voting with real production workloads rather than benchmark opinions.

The mechanism is simple, and it isn't loyalty, it's arithmetic. DeepSeek's V4 Flash model lists at roughly $0.14 per million input tokens against $5 for both GPT-5.6 Sol and Gemini 3.1 Pro, and its output pricing runs closer to a hundredth of Claude Opus 4.8's. One automation startup told CNBC it moved its entire traffic load from Claude to DeepSeek and expects the switch to save millions annually. Another saw its usage of a Chinese model grow 27-fold in a single week after switching. When a task doesn't need the absolute best model, and increasingly it doesn't, teams route it to the cheapest one that's good enough.

Timing made this sharper than it might otherwise have been. When Anthropic's most capable models were briefly taken offline in June under a US export control order, some enterprises had no transition period and no fallback plan. Several turned to Chinese alternatives out of necessity rather than preference, and stayed once they saw the invoice. Regulation didn't cause the shift toward cheaper models. It compressed a decision that was already happening into a single afternoon for a handful of large users.

The capability gap closed faster than the benchmarks suggest

On SWE-bench Verified, Claude's top model scores 95%. The strongest Chinese open-weight coding models sit in the high 70s to low 80s. Real, but a rounding error next to where things stood eighteen months ago, when DeepSeek's R1 first showed a Chinese lab could match Western reasoning quality at all.

Alibaba's Qwen family has separately become the most-downloaded open-weight model series on Hugging Face on the planet, built through sheer distribution rather than one flashy headline number. Moonshot AI's Kimi K2.5 reportedly came close to Claude Opus-class output on early benchmarks at roughly a seventh of the price. Four of the five most-used open-weight models globally are Chinese now, a lineup that didn't exist in this form two years ago.

If the frontier labs lose pricing power, who wins

Money doesn't disappear when pricing compresses. It moves.

Hyperscalers keep a share regardless of which model wins, since AWS, Azure and Google Cloud get paid for the compute either way, whether the workload runs on Claude, GPT, Gemini or DeepSeek. Enterprise software companies that wrap AI into a finished product can price on the outcome the product delivers rather than the tokens it consumes underneath, insulating them from the compression happening one layer down. Infrastructure and routing platforms, the OpenRouters of the world, take a toll on volume no matter whose model is fashionable that quarter, and volume is the one thing this shift is increasing for everyone.

The application layer, the businesses actually solving a customer's problem with AI rather than selling the AI itself, may end up the biggest beneficiary of all. Cheaper intelligence is an input cost for them, and a falling input cost usually means a bigger, not smaller, business built on top of it.

Why this matters for investors

This is a pricing power story before it's an AI story, and the mechanics work against the bull case quietly. If pricing compresses across the middle of the market, revenue growth can stay high and usage can keep exploding while margins decline anyway. Investors often mistake revenue acceleration for durable pricing power. They are not the same thing.

The next two quarters will say more than the next benchmark release. Watch what the frontier three do with API pricing on their mid-tier models rather than their flagships, since that's where the real volume sits. Watch enterprise renewal terms for volume discounts and multi-model routing clauses, the tell that a customer is shopping on price rather than staying on loyalty. Watch gross margins in the next funding disclosures, or in AI-segment reporting from public parents like Alphabet and Microsoft. And watch inference cost trends at the hyperscaler level: falling per-token costs paired with flat pricing is margin expansion, falling costs paired with falling prices is commoditization.

None of this means the frontier labs are losing the AI race. They may well keep building the world's most capable systems for years. If pricing continues to compress, though, the frontier labs could become less profitable than current expectations imply, and that is a different risk than the market is currently pricing in.

The distinction that will define the next phase

The bull case for the frontier labs' valuations has always rested on a durable moat: pay a premium because nothing else comes close. That premise gets harder to defend every time a free or near-free alternative clears the bar for the job at hand.

Technology leadership creates headlines. Pricing power creates shareholder returns. The next phase of AI may be decided by the second, not the first.

How we read the data

Curious how we get from raw data to a take like this? Our Trader's Toolkit walks through the tools we lean on.

Explore the Toolkit